Blockchain is easiest to understand as a shared ledger that multiple parties can trust without trusting a single party to edit the “master spreadsheet.”

That sounds abstract until you map it to real workflows: multi-company supply chains, shared audit trails, asset tracking, or any process where reconciliation is slow, and disputes are common.

Quick take (read this first)

- Blockchain is great at tamper-evident recordkeeping across multiple organisations—if you can govern who writes what and when.

- Blockchain is not magic privacy; putting personal data on-chain can create long-term compliance headaches.

- “Immutable” usually means you correct errors by adding new records, not editing old ones.

- Most business value is operational (auditability, reconciliation, traceability), not “faster payments” or hype. Claims about instant settlement often appear in consumer-facing industries—including marketing for fast payout gaming sites—but settlement speed depends more on system design and governance than on the word “blockchain” itself.

What blockchain actually is (no hype)

At a technical level, a blockchain records transactions in blocks, links those blocks using cryptographic hashes, and distributes copies of the ledger across nodes in the network.

As new blocks are added, older blocks become more difficult to modify—so the ledger is designed to be tamper-evident and tamper-resistant rather than “unhackable.”

If you want a standards-style explanation you can quote in internal docs, start with NIST’s blockchain technology overview.

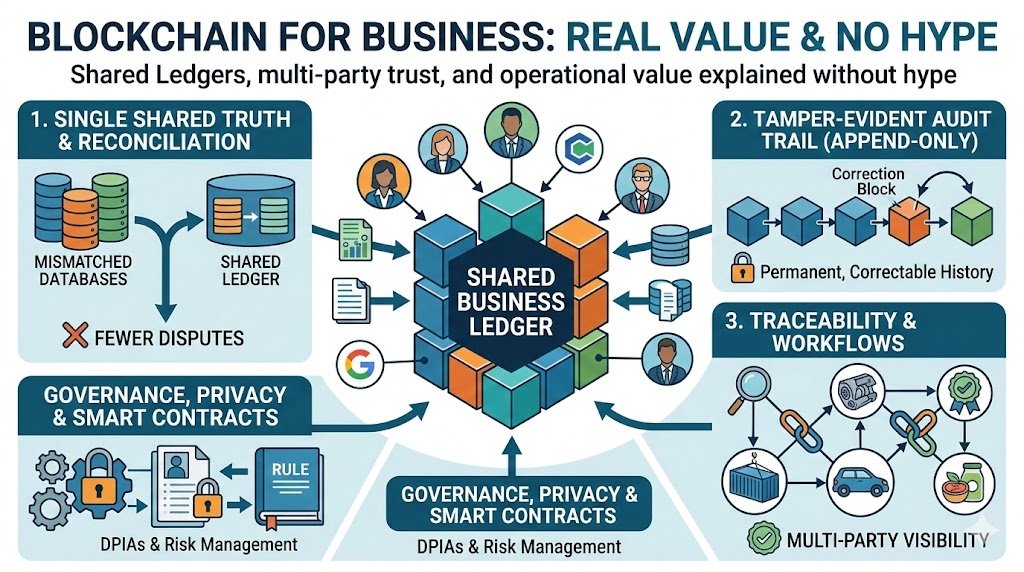

Why businesses use blockchain (the real value)

1) Shared source of truth (fewer reconciliation loops)

In classic multi-party workflows, each organisation keeps its own database, and teams spend time reconciling mismatches.

A shared ledger can reduce that “whose record is correct?” problem because all participants can reference the same history of recorded transactions.

How to verify: list the parties in your process, then count how many manual reconciliations happen per month and what they cost (time, delays, chargebacks, disputes).

2) Audit trails you can’t quietly rewrite

Append-only history is the point: when something is recorded, you typically don’t delete or overwrite it—you add a new transaction to correct or reverse it.

That’s useful for compliance and operations because you keep the “what happened” trail, including corrections.

If you need a plain-English business explanation of this “add a correcting record” model, IBM’s overview of what blockchain is in business networks spells it out clearly.

3) Traceability (with an important caveat)

Blockchain can improve traceability of events that participants actually record (shipments, custody changes, certifications), especially when several organisations need visibility.

The caveat: blockchain can’t prove real-world truth by itself—if someone records false data, the chain will preserve that false record very reliably.

How to verify: document your “source of truth” for inputs (scans, sensors, signed attestations) and define who is accountable for each data entry.

4) Automation via smart contracts (useful, but not a legal shortcut)

Many blockchain platforms support code-driven workflows (“smart contracts”) that can automatically execute steps when defined conditions are met.

That can reduce manual coordination, but it doesn’t automatically replace legal agreements, audits, or controls—you still need governance, testing, and change management.

How to verify: run a tabletop failure drill—what happens if a contract triggers wrongly, a key is compromised, or a data feed is wrong?

The part people skip: privacy, data protection, and “immutability” risks

If personal data goes on an immutable ledger, you may run into conflicts with data-protection expectations like storage limitation, rectification, and erasure—because the data can persist indefinitely.

The UK ICO explicitly flags that the permanent/immutable nature of blockchain storage can create compliance concerns when personal data is on-chain, and that re-identification risk can increase as more data accumulates.

Before you ship anything that touches user/customer data, read the UK ICO’s response on cryptoassets and data protection and align with your DPO/legal team.

How to verify (practical): keep personal data off-chain where possible, store references/hashes instead, and document retention/erasure handling as part of your DPIA (or equivalent privacy risk assessment).

Tokenisation: what it is (and what it isn’t)

Tokenisation is the process of generating and recording a digital representation of traditional assets on a programmable platform.

That can enable new ways to track ownership and automate transfers, but it’s also a regulatory and operational topic—not a “growth hack” for fundraising.

For a careful, non-marketing definition, use the BIS/CPMI report section that defines tokenisation in “Tokenisation in the context of money and other assets”.

If you operate in (or sell into) the UK, note that the FCA has been actively discussing tokenisation models and barriers; their fund tokenisation work is a good reality check on what’s “possible” versus “compliant.”

Decision framework: should you use blockchain or a normal database?

Blockchain is a strong candidate when…

- Multiple organisations need to write to the same record history, and you can’t rely on one party to be the forever-admin.

- You need an append-only audit trail where corrections are explicit transactions.

- Disputes today come from mismatched systems, unclear provenance, or slow reconciliation.

A normal database is usually better when…

- One organisation controls the whole workflow end-to-end (you mostly need good logging and access control).

- You must delete/rectify personal data reliably and quickly, and you can’t architect around on-chain permanence.

- Your core pain is performance tuning or UX—not multi-party trust and reconciliation.

If you want to turn this into an internal decision memo, use a simple “trust + writes” test: who needs write access, who audits, who can upgrade the rules, and what happens when parties disagree?

Implementation checklist (what a real pilot should include)

- Define participants and governance: who can write, validate, read, and change rules.

- Define the “correction model”: how you reverse mistakes without rewriting history.

- Define the privacy model: what never goes on-chain, retention rules, and how you handle data subject rights.

- Define input trust: how off-chain events become on-chain records (signatures, attestations, audits).

- Define exit paths: what happens if you migrate platforms or a consortium member leaves.

FAQ

Is blockchain “secure” by default?

It’s designed to make tampering with recorded history difficult and detectable, but security still depends on keys, software, governance, and what data you store.

Does blockchain guarantee privacy or anonymity?

No—privacy depends on architecture, and writing personal data on-chain can create long-term retention/erasure problems under data protection expectations.

How do you fix a mistake on a blockchain?

Typically by adding a correcting/reversing transaction rather than editing the original record, which preserves the audit trail.

Are smart contracts the same as legal contracts?

Not necessarily; they can automate execution of steps, but legal enforceability and controls are separate questions.

Is tokenisation just “putting assets on-chain”?

Conceptually it’s a digital representation of assets on a programmable platform, but the operational and regulatory details matter a lot in practice.

What’s the fastest way to evaluate blockchain fit?

Map your workflow, list parties and write access needs, price the current reconciliation/dispute costs, then run a small pilot with clear governance and privacy constraints.

💬 Comments